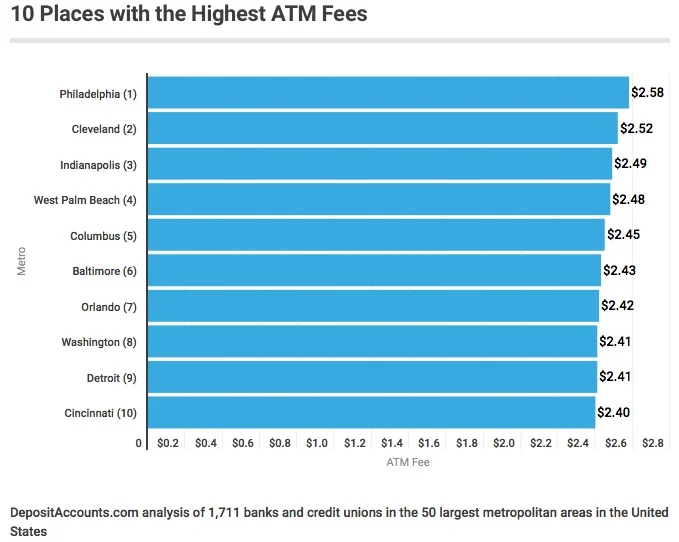

Study: Bank of America, M&T Bank, PNC, Wells Fargo Bank & Other "Banksters" are Charging the Highest Overdraft & ATM Fees in Cities with Large Black Populations

/

Harrisburg, PA 52% Black

Cleveland 53% Black

West Palm Beach 55% Latino & Black

Cincinnati 44% Black

Baltimore 64% Black

Atlanta 51% Black

Washington DC 51% Black

Detroit 81% Black

From [HERE] DepositAccounts.com’s conducted a study of checking account fee data from 1,711 banks and credit unions with branches in the 50 of the largest U.S. metro areas. Checking account fee data from online banks was also analyzed. The study focused on three of the common checking account fees: overdraft fees, third-party ATM fees and monthly service fees. [MORE]

Banks made $32 billion last year in overdraft fees alone. Overdrafts are one of the most expensive ways to "borrow money" in the world.

- Banks charge effective APRs > 1,000% – making them worse than payday lenders

- Banks have purposefully made the system obscenely complex.

- Banks regularly re-order transactions in the background, increasing the fees you pay and stacking the deck against you

It’s Thursday, the day before payday. You only have $50 left in checking and have forgotten that your gym membership of $70 will be automatically debited from your account today. Normally, you’d transfer a little bit out of savings to cover the cost if you needed to, but you didn’t do it in time. The bank approved your gym’s charge and now your balance is negative $20.

The bank has 2 choices: approve the transaction or decline the transaction.

If they approve the transaction, then you go overdraft and will be charged an overdraft fee. The average fee is about $35 per incident. You can be charged multiple times a day. One of the worst examples is Citizens Bank, which charges $37 per incident, up to a shocking 7 incidents per day - that’s $259 in fees for a single day!

When your account is overdrawn, the balance is negative. You have to bring the balance positive (by putting money into the account), or else you will be charged an extended overdraft fee.

At Bank of America, you would be charged another $35 if the account is negative for 5 days. And remember: you have to cover both the amount you borrowed and the fee. In the case of the gym membership – you would have to pay the $20 you borrowed and the $35 fee in 5 days, otherwise you are charged another $35!

If the bank decides to decline the transaction, you still get charged a fee. This fee is called an NSF fee aka non-sufficient-funds fee. And, guess what? The fee is still a shocking $35 per incident.

So: you are charged $35 if it is approved or declined. Bank of America will charge $35 even if the overdraft was less than $10.

In a normal world, transactions that take place at 8AM will be deducted from your checking account at 8AM. Unfortunately, the rules are stacked against you. Rather than posting the transactions when they actually happened, a lot of banks post transactions when they wish they would have happened.

Nearly 50% of banks use what is called “high to low processing.” They take all of your transactions from the day, and deduct them from your account from highest amount to lowest amount (and they do this at the end of the day). That means you will go overdraft sooner, and you will pay more fees.

Imagine you have a balance of $50. You have 2 transactions: a morning trip to Starbucks for $5, and then dinner for $55. If the transactions were posted in order, then you would only have one overdraft transaction: the dinner for $55.

If the transactions were posted from high to low (and not in the order they happen), then you would have 2 overdraft transactions! At an average bank, that would increase the fee from $35 to $70! [MORE]

And that is perfectly legal by "banksters."

Philadelphia, PA 56% Black & Latino